Insurance Claims for Roofs in Texas: How to Avoid Common Denials

Understanding Your Texas Roof Insurance Policy

Filing a roof insurance claim in Texas can be confusing. Understanding the process and common pitfalls helps you avoid denials and maximize your coverage. Let's break down exactly what you need to know. For a comprehensive understanding of the claims process, see our detailed guide on how roofing insurance claims really work.

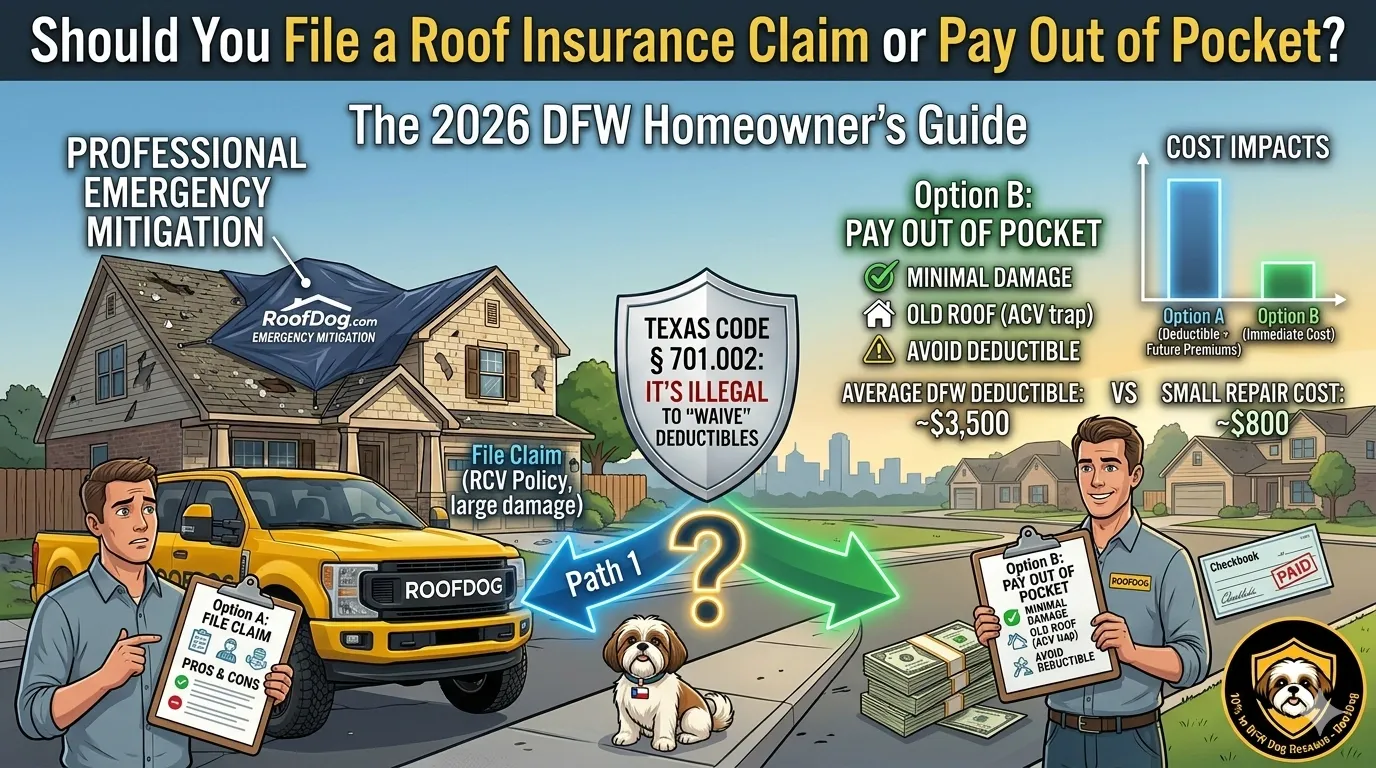

ACV vs. RCV: What's the Difference?

Replacement Cost Value (RCV)

RCV pays to replace your damaged roof with a new one of similar quality, regardless of your old roof's age. This is the most comprehensive coverage and what most newer policies provide.

Example: Your 10-year-old roof needs replacement. An RCV policy pays for a complete new roof installation (minus your deductible), even though your old roof had depreciated.

Actual Cash Value (ACV)

ACV pays the replacement cost MINUS depreciation. The older your roof, the less you receive.

Example: Same scenario, but with ACV coverage. Your insurance values the replacement at $20,000, but your 10-year-old roof is depreciated at 50%. You receive $10,000 minus your deductible — potentially leaving you thousands short.

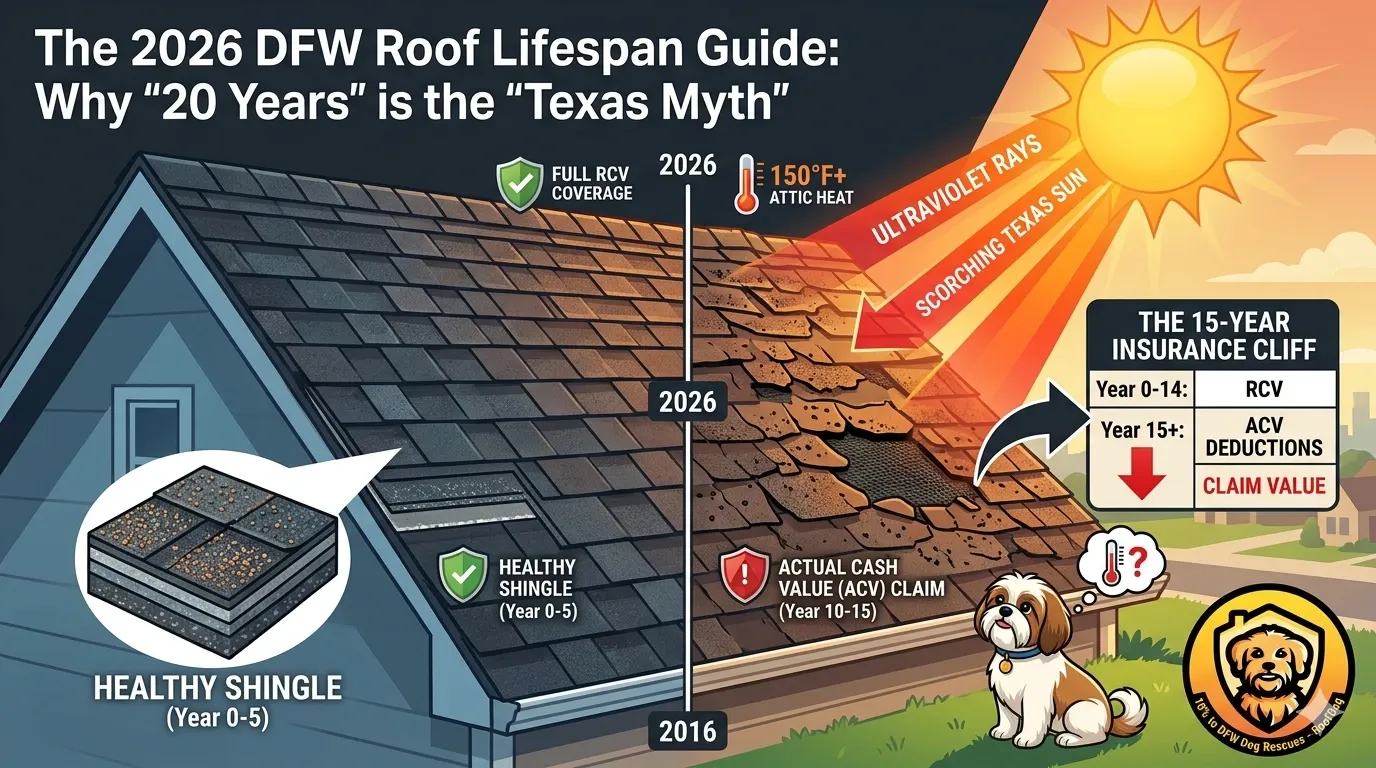

How Depreciation Works in Texas

Even with RCV policies, insurance companies withhold depreciation until work is completed. Here's the typical process:

- Claim approval: Insurance agrees to pay $20,000 for your roof

- First check (ACV): You receive $12,000 (after depreciation and deductible)

- Installation complete: Contractor finishes work and you submit final invoice

- Second check (depreciation): Insurance releases the remaining $8,000

Top Reasons for Texas Roof Claim Denials

1. "The Damage is From Normal Wear and Tear"

Insurance covers sudden, accidental damage — not gradual deterioration. If your roof is simply old and worn out, your claim will be denied.

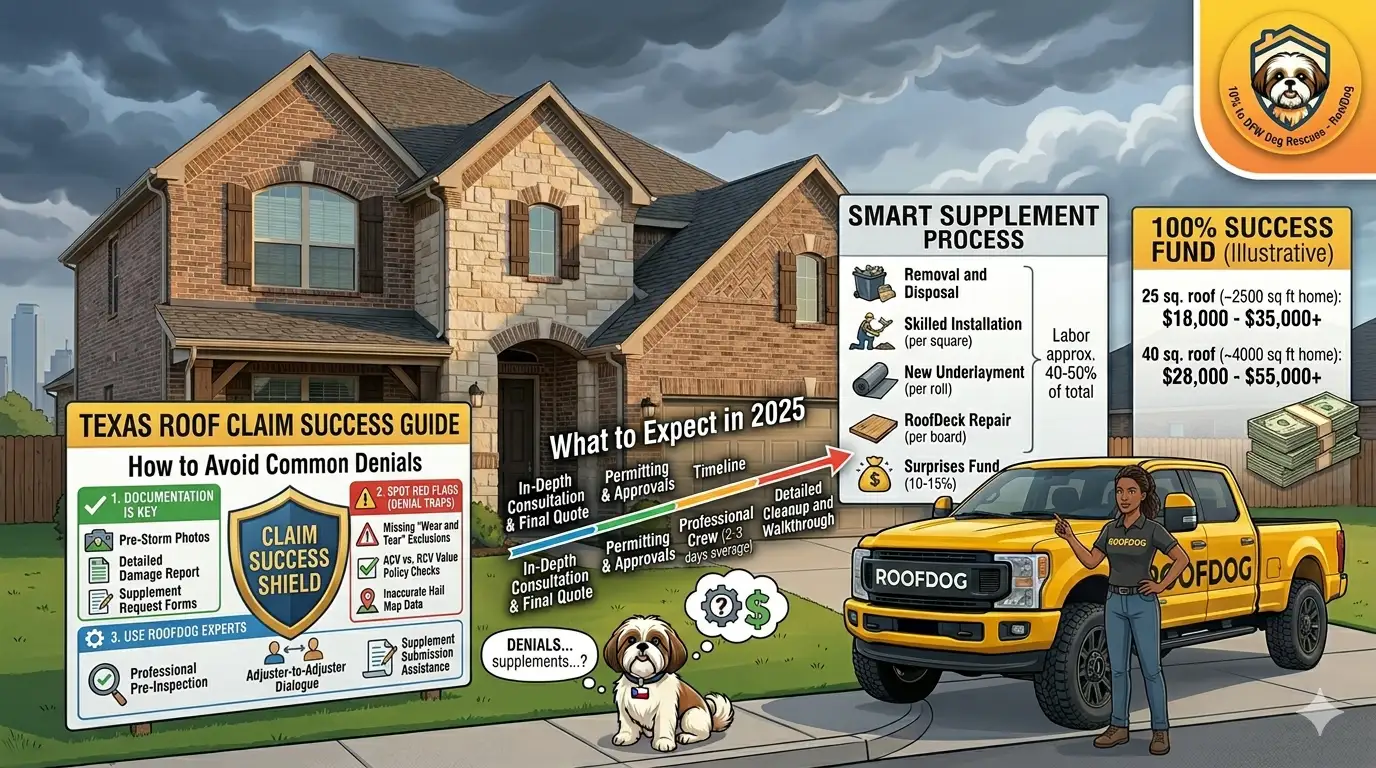

How to avoid this: Document the storm date and ensure damage is clearly tied to a specific hail or wind event. Professional inspections that note distinct impact patterns help prove storm damage vs. age.

2. "Pre-Existing Damage"

If your roof had damage before the covered event, insurers may deny your new claim.

How to avoid this: Don't delay filing after storms. The longer you wait, the harder it is to prove when damage occurred. File within 30 days of discovering damage.

3. "Inadequate Maintenance"

Policies require homeowners to maintain their property. Severe neglect can void coverage.

How to avoid this: Perform basic maintenance: keep gutters clean, replace missing shingles promptly, ensure proper ventilation. Document maintenance with photos and receipts.

4. "Below Threshold for Coverage"

Many insurance companies require a minimum number of hail impacts per "test square" (usually 8-12 impacts per 100 sq ft) to approve full replacement.

How to avoid this: Have an experienced contractor present during the adjuster's inspection. They can help identify and document all damage, ensuring nothing is missed.

5. "Cosmetic Damage Only"

Some policies exclude "cosmetic" damage that doesn't affect functionality. This particularly applies to metal roofs with hail dimples.

How to avoid this: Review your policy for cosmetic damage exclusions BEFORE you need to file. If you have this exclusion, consider removing it at renewal.

Working Effectively with Insurance Adjusters

Your Rights as a Policyholder

- You can have your contractor present during inspections

- You can request a supervisor review if you disagree with findings

- You can hire a public adjuster (though they take 10-15% of your settlement)

- You can request a written denial explanation if your claim is rejected

Best Practices

- Be present: Don't let the adjuster inspect alone. Ask questions and take your own photos.

- Document everything: Keep copies of all correspondence, photos, estimates, and invoices.

- Know your policy: Read your coverage details, deductible, and depreciation structure before filing.

- Don't accept first offer immediately: If you believe the estimate is too low, you can negotiate or request re-inspection.

- Use a local, reputable contractor: Storm chasers who overstate damage hurt legitimate claims. Work with established local contractors who document honestly.

Why Contractor Choice Matters

Your roofing contractor plays a critical role in claim success. Here's what reputable contractors provide:

- Accurate damage assessment: Not inflated, not minimized — just honest documentation

- Detailed estimates: Line-item estimates that match insurance requirements

- Claim support: Help with documentation, adjuster meetings, and supplement requests

- Quality workmanship: Installations that pass inspections and honor warranties

- Long-term presence: They'll be here for warranty work and future needs

Learn more about how to choose a roofing contractor you can actually trust.

Storm Chasers Hurt Your Claim

Unlicensed "storm chasers" who flood your neighborhood after weather events often:

- Overstate damage, causing insurance companies to scrutinize everything

- Pressure you to sign contracts immediately

- Disappear after taking deposits

- Do substandard work that fails inspections

- Leave you holding the bag when warranty issues arise

What To Do If Your Claim is Denied

- Request detailed written explanation: Insurance must explain specifically why they denied

- Review the denial: Is it legitimate (age/wear) or disputable (missed damage)?

- Get a second inspection: Have another contractor review the adjuster's assessment

- Request re-inspection: Provide additional documentation and request another look

- Consider a public adjuster: For large claims, a public adjuster may be worth the 10-15% fee

- File a complaint: Texas Department of Insurance handles disputes between homeowners and insurers

Frequently Asked Questions

Can my insurance company drop me after filing a roof claim?

Not typically after one weather-related claim. Texas regulations protect homeowners from cancellation solely due to weather claims. However, multiple claims in 3-5 years can affect renewability.

Should I file a claim if I'm not sure there's damage?

Get a professional inspection first. Filing a claim goes on your record even if nothing is found. Have an expert verify damage exists before filing. For severe weather events, also read our step-by-step guide for dealing with hail damage.

What's a "supplement" and when do I need one?

A supplement is a request for additional payment when the insurance estimate is insufficient. This is common when hidden damage (like rotted decking) is discovered during installation. Reputable contractors handle supplements as part of their service.

How long does the claim process take?

From filing to completion: typically 4-8 weeks. This includes adjuster visit (1-2 weeks), estimate receipt (1 week), installation scheduling (1-3 weeks), and depreciation recovery (1-2 weeks after completion).

Get Expert Help with Your Texas Roof Claim

RoofDog has helped thousands of North Texas homeowners successfully navigate insurance claims. We provide honest damage assessments, work directly with your insurance company, and ensure you receive fair compensation.

Call (214) 490-7073 for a free inspection and claim consultation. We'll review your damage, explain your coverage, and guide you through every step.

Need a Roof Inspection?

Get expert advice and a free estimate from North Texas's trusted roofing professionals.

Schedule Free Inspection