Why More Texas Insurance Companies Are Restricting Roof Coverage in 2026

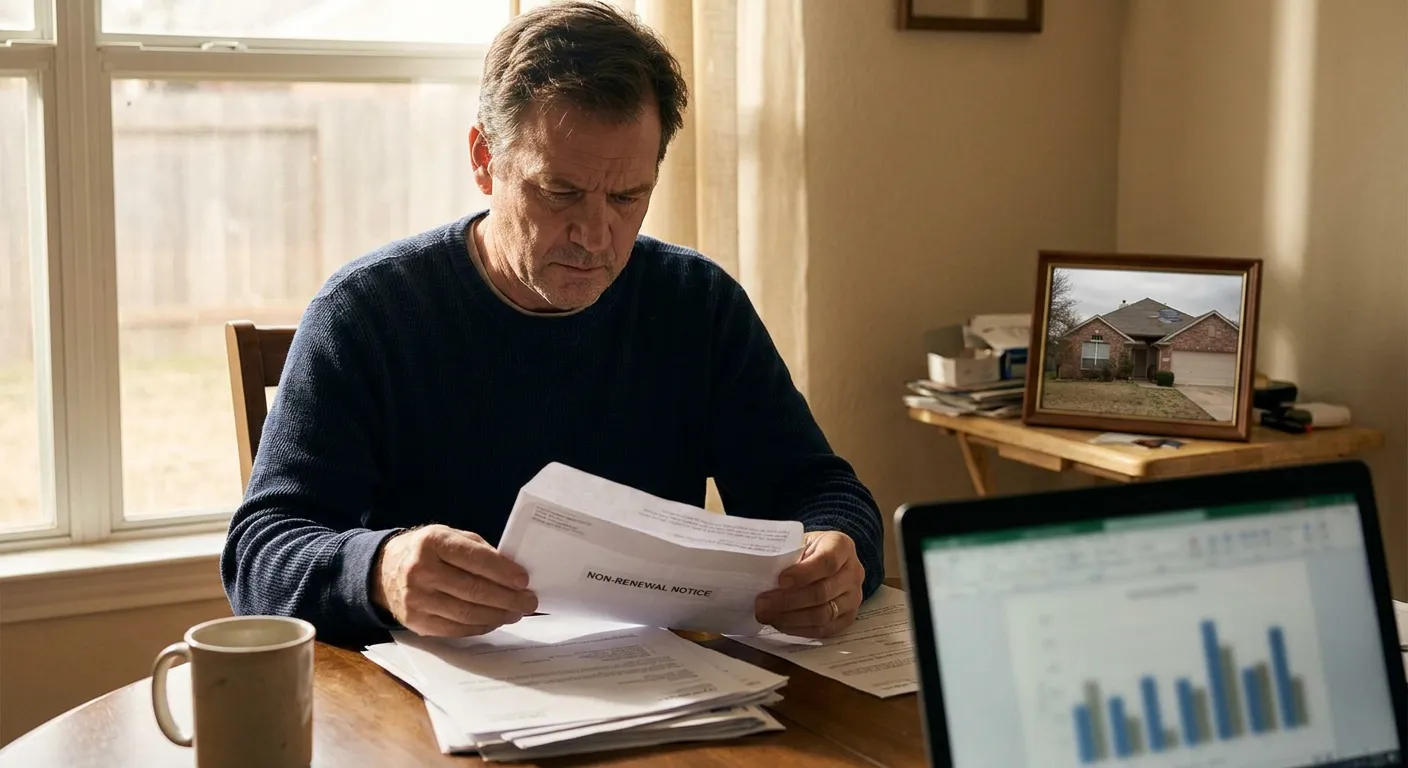

As we navigate through the midpoint of 2026, homeowners in the Dallas-Fort Worth metroplex and across the Lone Star State are waking up to a stark new reality: the Golden Age of Texas roofing insurance is officially over. For decades, North Texas was the land of the free roof, where a single hailstorm meant a brand-new roof for a relatively small deductible. However, a combination of climate-related losses, global reinsurance hikes, and shifting actuarial models has led to a seismic shift. Texas roof insurance changes are no longer just industry rumors—they are reflected in the non-renewal notices and policy updates hitting mailboxes every day.

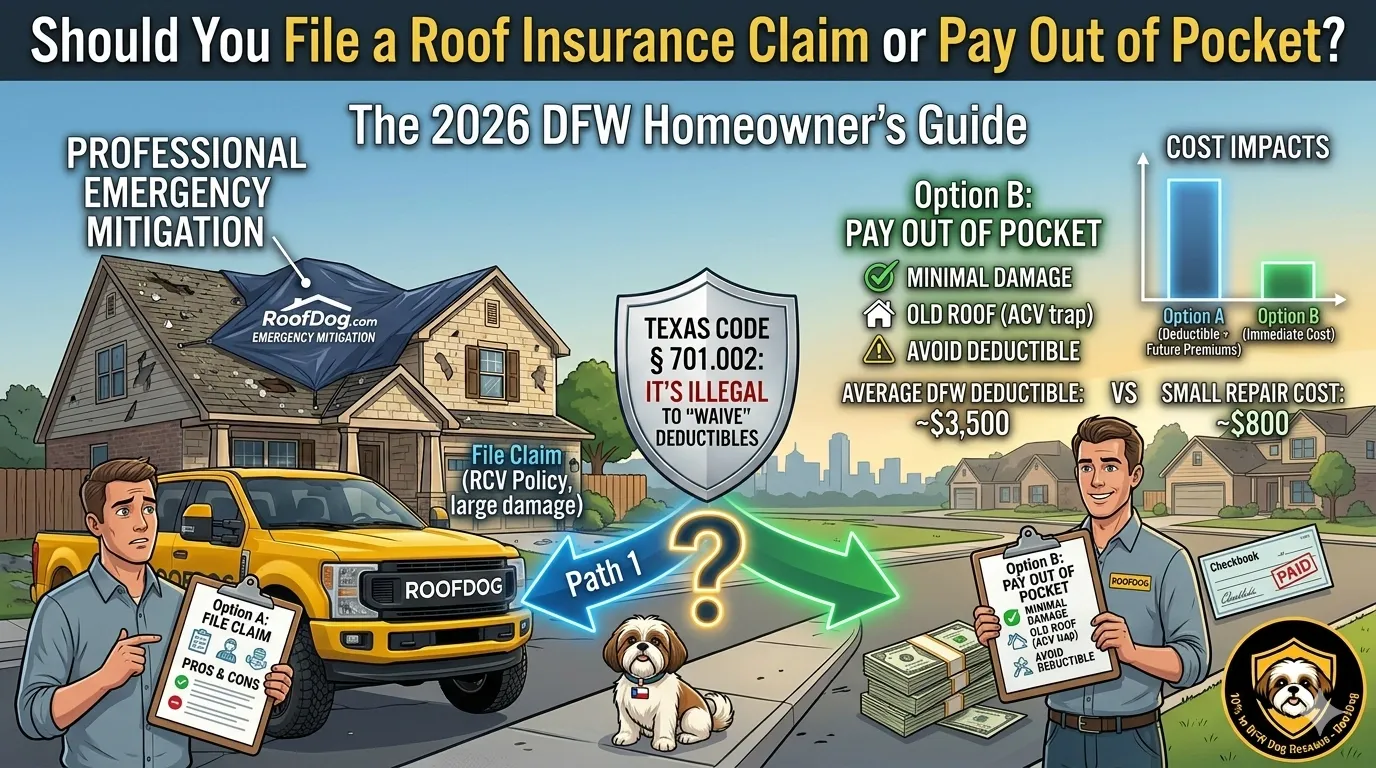

If you have recently had a roof insurance denied or noticed that your premiums have spiked by 30% or more, you are not alone. Insurance carriers are in survival mode. The sheer volume of billion-dollar weather events in Texas over the last five years has forced them to implement roof coverage restrictions that were unheard of just a decade ago. In this comprehensive 2026 guide, we will break down exactly how these changes affect you, what an ACV roof policy in Texas actually means for your wallet, and the specific insurance roof exclusions you need to watch for before the next storm hits. For a primer on how the modern claim process works, start with our roofing insurance claims guide.

1. The Rise of the ACV (Actual Cash Value) Policy

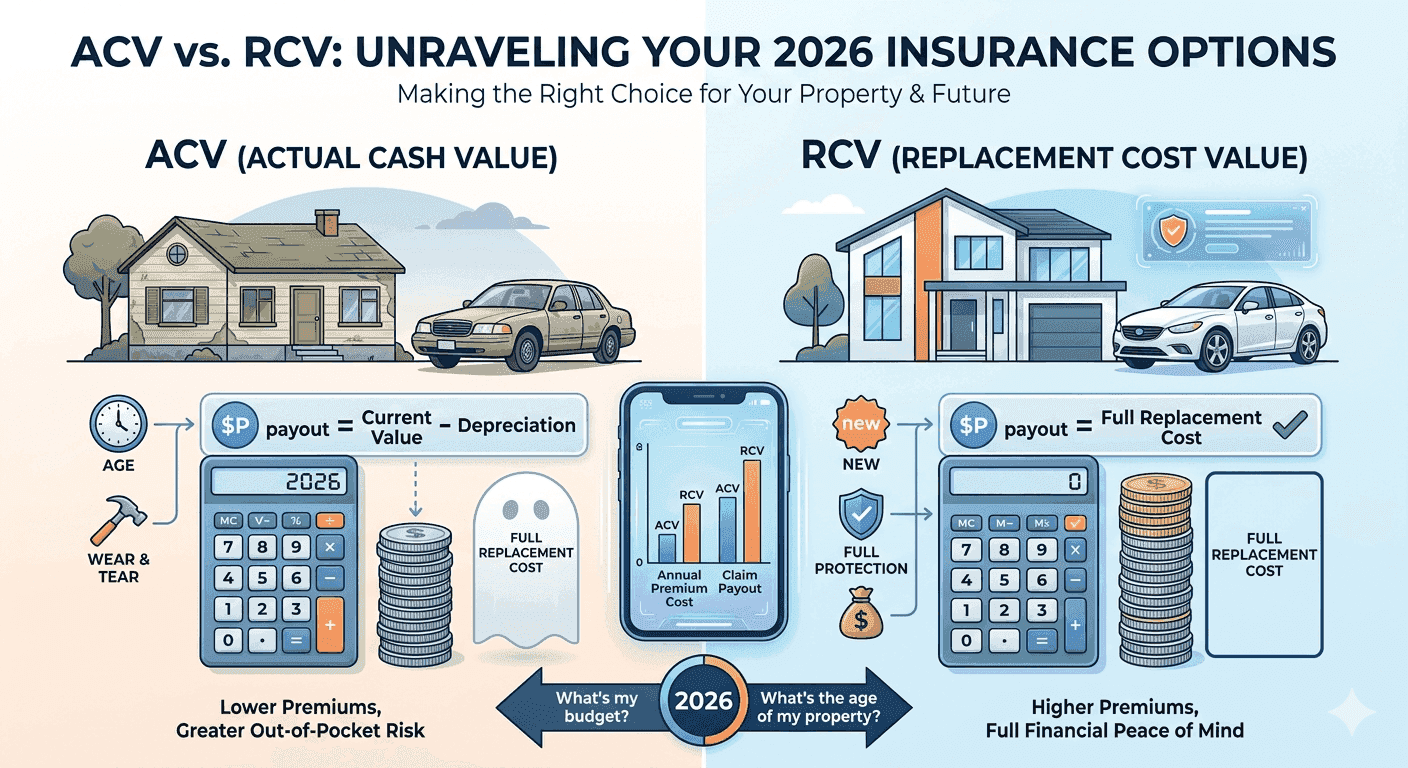

The biggest change in the 2026 market is the transition from Replacement Cost Value (RCV) to Actual Cash Value (ACV) for roofs. Historically, most Texas policies were RCV, meaning the insurance company paid to replace the roof with new materials, regardless of the old roof''s age. If you had a 20-year-old roof, insurance would buy you a brand-new one today.

An ACV roof policy in Texas works differently. Under ACV, the insurance company depreciates the value of your roof based on its age. If your shingles have a 30-year lifespan and the roof is 15 years old, the insurance company will only pay 50% of the cost of the materials. The other 50% must come out of your pocket, in addition to your deductible. Many carriers in 2026 are making ACV mandatory for any roof older than 10 or 15 years. This transition is responsible for the majority of the sticker shock homeowners experience after a claim. We dove deeper into this exact transition in our breakdown of the 2026 Texas ACV insurance shift.

2. Cosmetic Exclusions: When "Ugly" Isn''t "Damaged"

Perhaps the most frustrating of the new insurance roof exclusions is the Cosmetic Damage Waiver. In 2026, many carriers have introduced language that excludes coverage for damage that only alters the appearance of the roof but does not impact its functional performance or ability to shed water.

What does this mean for a DFW homeowner? Imagine a hailstorm pummels your metal roof or your expensive clay tile. The hail leaves deep, unsightly pits and dents that diminish the curb value of your home. However, because the roof isn''t leaking and the shingles haven''t been fractured to the point of water penetration, the insurance company can legally deny the claim under a cosmetic exclusion. This change has made roof insurance denied reports more common for high-end roofing materials, leaving homeowners with depreciated assets that insurance won''t fix. If you are unsure whether your damage is cosmetic or functional, our companion piece on why one house needs a replacement and yours may not walks through the forensics adjusters use.

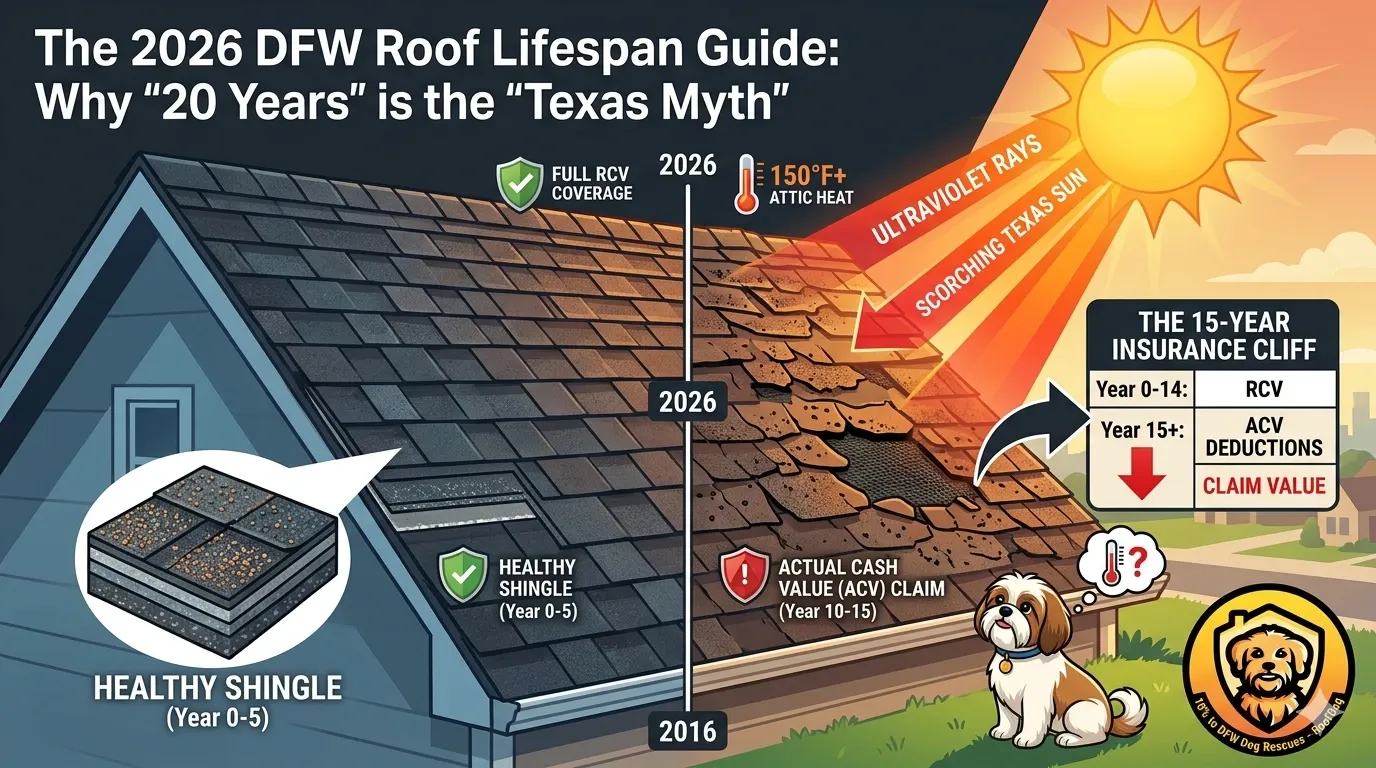

3. The "Roof Age" Hard Cutoff

In 2026, we are seeing roof coverage restrictions tied directly to the calendar. Many major Texas insurers are now refusing to write new policies on homes with roofs older than 15 years. Some are even issuing mandatory non-renewal notices unless the homeowner can prove the roof has been replaced within the last decade. This age-based restriction is a defensive move against the inevitable degradation of asphalt shingles in the Texas sun. As a result, the value of a professional roof replacement has shifted—it''s no longer just about protecting your house; it''s about keeping your home insurable at all. Our DFW roof lifespan and insurance age trap post covers the new actuarial timelines.

Important for DFW Residents: If your roof was installed before 2012, you are in a high-risk category for policy cancellation in 2026. Carriers are using satellite imagery and AI to triage neighborhoods, identifying old roofs from the air and sending out notice letters before a storm even occurs. A documented professional roof inspection is one of the strongest tools you have to push back.

4. Changing Deductible Structures: The 2% Reality

For years, a 1% deductible was the standard. On a $400,000 home, that was a manageable $4,000. In 2026, many Texas roof insurance changes include a mandatory Wind/Hail Deductible of 2% or even 3%. On that same home, a 2% deductible means you are on the hook for $8,000 before the insurance company pays a single cent. This shift effectively turns the insurance policy into a catastrophe-only plan, where the homeowner bears the majority of the risk for mid-sized storms. If a storm hits and you need to bridge that gap, our roof financing options are designed to keep you covered without draining savings.

5. Mandatory Impact-Resistant Shingles

Carriers are now nudging homeowners toward better materials through both carrots and sticks. Some insurers will only offer RCV coverage if the homeowner agrees to install Class 4 Impact-Resistant shingles. Others are offering significant premium discounts (up to 25%) for these materials. In 2026, the cost-benefit analysis has changed; the extra $1,500-$2,500 spent on a Class 4 roof usually pays for itself in insurance savings within three years, not to mention the added protection against roof coverage restrictions in the future. Pair these shingles with the right attic ventilation and you have one of the most resilient roof systems money can buy in North Texas.

6. The Impact of Global Reinsurance

Why is this happening in Texas specifically? It''s not just about local storms. Texas is part of a global reinsurance pool. Reinsurance companies (the companies that insure the insurance companies) have seen record payouts due to wildfires in California, hurricanes in Florida, and the perennial hail in North Texas. These global firms have raised their rates for Texas-based carriers, who then pass those costs and roof coverage restrictions down to the consumer. In 2026, your roofing policy is being influenced by events happening half a world away.

7. The Rise of "Limited Matching" Clauses

One of the more subtle insurance roof exclusions appearing in 2026 policies is the Limited Matching or Line of Sight clause. Historically, if a hailstorm damaged one side of your roof and that specific shingle was discontinued, Texas law often forced the insurance company to replace the entire roof so that it matched. New policy language is bypassing this, stating the company only has to replace the damaged slope, even if the new shingles don''t match the rest of the house. This can leave a home with a patchwork roof that kills resale value. Compare adjusters'' carve-outs against an apples-to-apples bid using our how to compare roofing estimates guide.

How to Protect Yourself in this New Market

With all these Texas roof insurance changes, homeowners must be proactive. Here is the RoofDog strategy for 2026:

- Audit Your Policy Annually: Don''t just auto-renew. Look for words like Actual Cash Value, Cosmetic, and Matching.

- Invest in Class 4 Materials: It is the only way to future-proof your insurability in North Texas. See our deep-dive on Class 4 impact-resistant shingles.

- Document Everything: Keep a Roof Portfolio with photos of the installation, invoices, and annual maintenance reports. This proves to the carrier that the roof is well-maintained and not just a deferred maintenance liability.

- Work with Informed Contractors: You need a local DFW roofer who understands the latest Xactimate pricing and policy shifts. A truck and ladder guy won''t know how to navigate a complex ACV claim. Vet candidates with our how to choose a roofing contractor guide.

Conclusion: The New Frontier of Texas Roofing

The changes we are seeing in 2026 are not temporary. They represent a fundamental restructuring of how risk is shared between the homeowner and the insurance giant. While it is more difficult than ever to get a roof insurance denied reversed or to find full RCV coverage, being informed is your best defense. At RoofDog, we stay ahead of these roof coverage restrictions to ensure our clients aren''t left holding the bill for a storm they didn''t ask for. We are moving into a future where quality materials and legal knowledge are just as important as a good hammer.

If you''re ready for an honest assessment of your roof''s age, condition, and insurability, schedule a free inspection or contact RoofDog today. We''ll give you the documentation and the strategy to keep your home insurable through whatever 2026 has left to throw at us.

You Might Also Need

- Roofing insurance claims guide →

- 2026 Texas ACV insurance shift →

- Why one house needs replacement and yours may not →

- Roof replacement →

- DFW roof lifespan and insurance age trap →

- Professional roof inspection →

- Roof financing options →

- Class 4 impact-resistant shingles →

- Attic ventilation →

- Compare roofing estimates →

- Roof maintenance →

- Local DFW roofer →

- How to choose a roofing contractor →

- Schedule a free inspection →

- Contact RoofDog →

Need a Roof Inspection?

Get expert advice and a free estimate from North Texas's trusted roofing professionals.

Schedule Free Inspection