Should You File a Roof Insurance Claim or Pay Out of Pocket? The 2026 DFW Homeowner's Guide

In the wake of a North Texas storm, the immediate reaction for most homeowners is to reach for their phone and dial their insurance agent. It makes sense — you pay thousands of dollars in premiums every year specifically to protect your home from the volatile DFW weather. However, in 2026, the question of "should I file a roof claim" has become significantly more complex. Between rising premiums, changing deductible structures, and the long-term impact on your insurability, the decision to use your insurance policy is a major financial crossroads.

This comprehensive guide is designed to help you navigate the claim vs cash pay dilemma. We will break down the math, the risks, and the strategic advantages of each path. Is a roof deductible worth it in the current market? Does an insurance claim increase premiums enough to offset the payout? By the end of this deep dive, you will have the clarity needed to decide if your roof damage is worth claiming — or if you are better off keeping the insurance company out of it entirely. This isn't just about getting a new roof; it's about protecting your long-term financial health in one of the most difficult insurance markets in Texas history.

The Math of the Deductible: Is It Worth It?

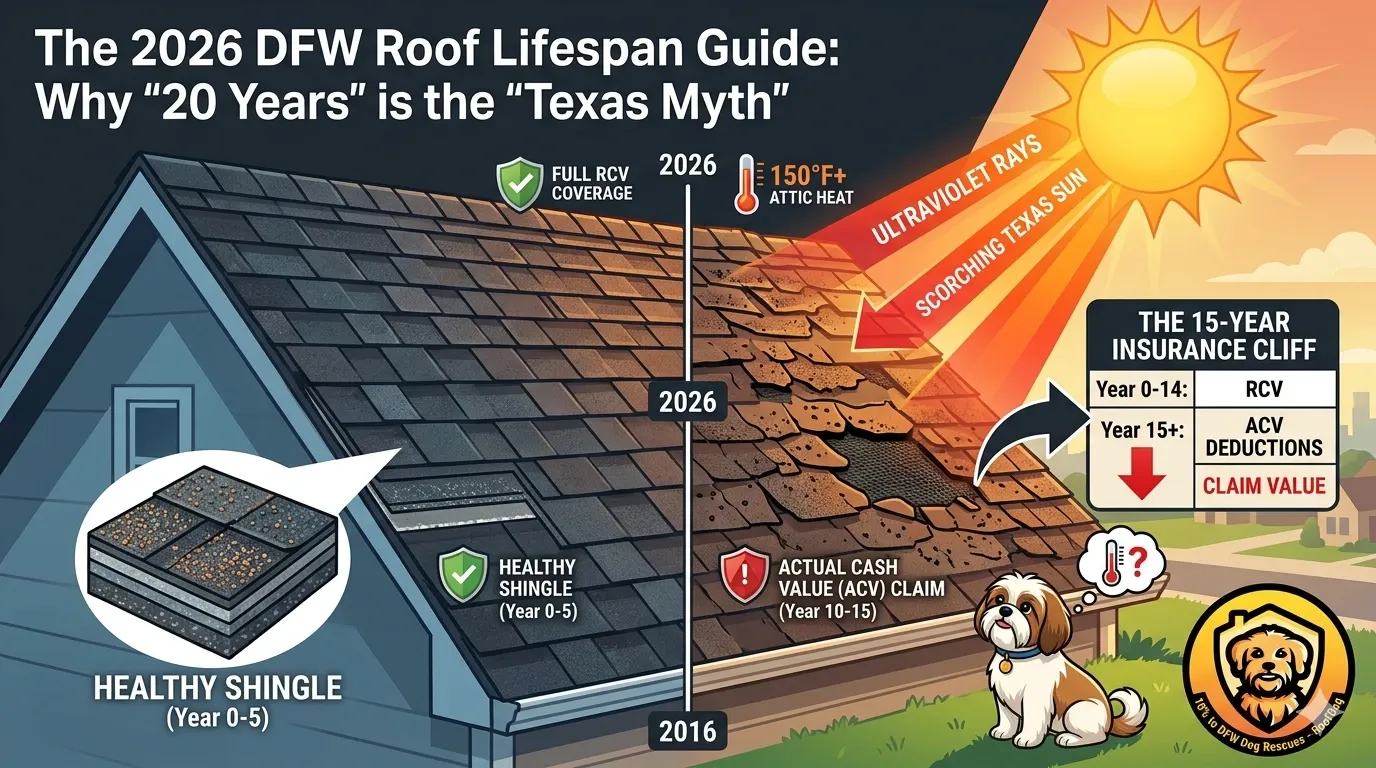

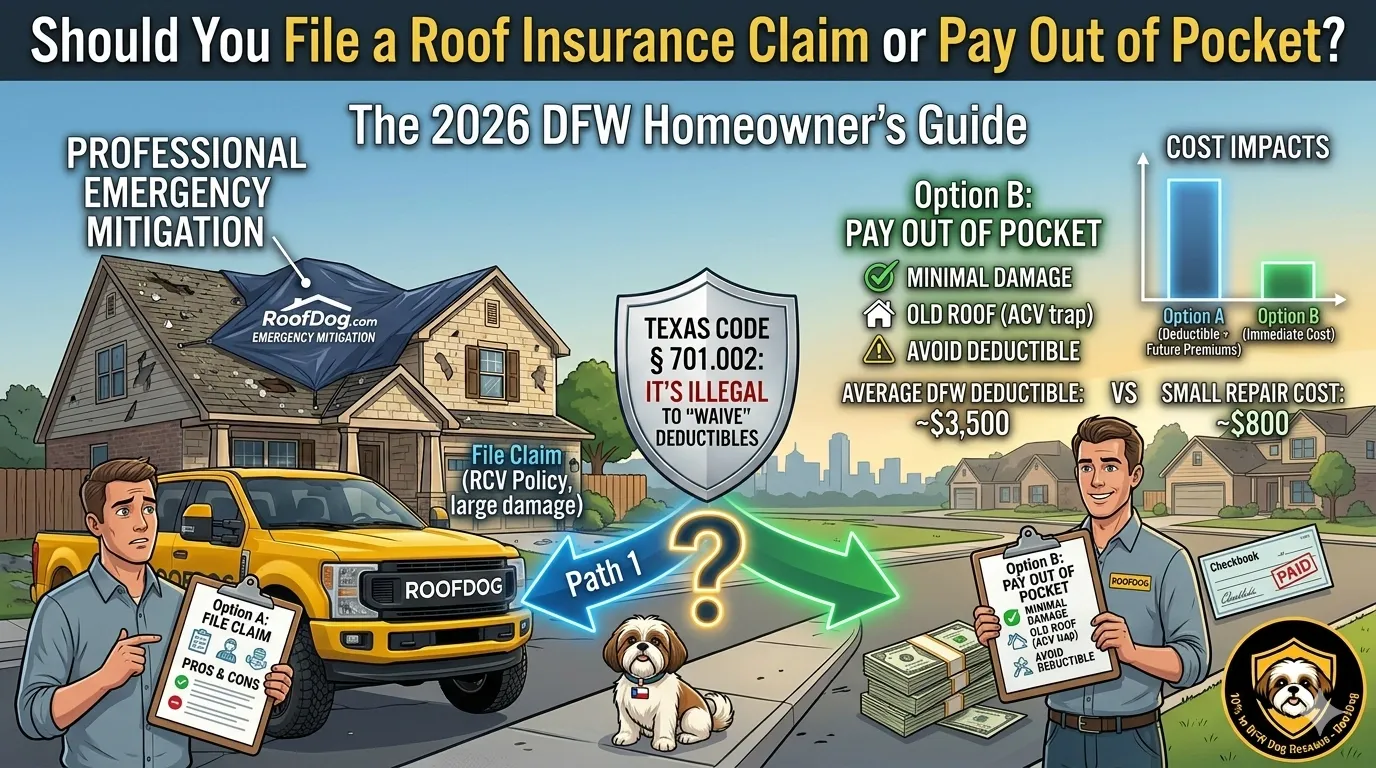

The first and most important factor in this decision is your deductible. In recent years, Texas carriers have shifted many homeowners from a flat dollar amount to a percentage-based deductible for wind and hail. If your home is insured for $500,000 and you have a 2% wind/hail deductible, you are responsible for the first $10,000 of any roof replacement.

The roof deductible worth it calculation starts with the total cost of the project. If a high-quality roof replacement costs $14,000 and your deductible is $10,000, the insurance company is only contributing $4,000. While $4,000 is not a small amount of money, you must weigh that against the potential downsides. Filing a claim for a relatively small net payout can be a strategic error. In the eyes of an insurance carrier, a "claim is a claim," regardless of whether they pay out $4,000 or $40,000. If you have another claim in the next three years, you may find yourself facing non-renewal or a massive premium hike that far exceeds the $4,000 you "saved."

Strategic Pay Out of Pocket: The "Cash Pay" Advantage

When you choose the claim vs cash pay route and opt for the latter, you gain several advantages that insurance-funded jobs lack. First is the speed and simplicity. You aren't waiting weeks for an adjuster, negotiating over line items in Xactimate, or dealing with "depreciation" holdbacks. You are the boss. This allows for immediate emergency tarping and faster permanent repairs, which prevents secondary damage like mold or wood rot.

Furthermore, cash-pay customers often have more flexibility in material selection. When insurance pays for a roof, they typically pay for "like kind and quality." If you have basic 3-tab shingles, they pay for basic 3-tab shingles. If you want to upgrade to Class 4 impact-resistant shingles (which we highly recommend for DFW), you have to pay the difference anyway. By paying out of pocket, you can negotiate a direct "package deal" with your contractor that includes upgrades, better ventilation, and extended labor warranties that aren't tied to an insurance carrier's rigid pricing model.

Will an Insurance Claim Increase My Premiums?

This is the most common question we hear: "insurance claim increase premiums?" In Texas, the law (Texas Insurance Code Section 544.352) technically prohibits carriers from increasing your rates solely because you filed a single claim for damage caused by a "natural cause" like hail or wind. However, there is a massive caveat: they can — and do — increase rates for an entire ZIP code or geographic area based on storm frequency.

More importantly, carriers use "claim frequency" as a metric for risk. If you file a claim today for minor hail damage and another claim in two years for a kitchen fire, the carrier may view you as a "high-risk" policyholder. This leads to the loss of "claim-free discounts," which can represent 10–20% of your annual premium. Over five to ten years, the loss of that discount can cost you thousands of dollars. When asking if roof damage is worth claiming, you must look at the 10-year total cost of ownership, not just the immediate repair bill.

The "Zero-Pay" Trap: Many homeowners don't realize that calling your insurance to "just have them take a look" can count as a claim on your CLUE report, even if they pay out $0. Always have a reputable roofing contractor perform a private inspection first to determine if the is roof damage worth claiming threshold has actually been met.

When You SHOULD Definitely File a Claim

While we advocate for caution, there are times when filing a claim is absolutely the correct move. These include:

- Catastrophic Damage: If a tornado or severe wind event has removed large sections of your roof, the cost of repair will far exceed any deductible.

- Internal Leaks: If water is entering the home and damaging ceilings, insulation, and electronics, you are dealing with a multi-part claim that requires professional remediation.

- Full Replacement Needs: If your roof is at the end of its lifespan and has sustained legitimate, functional hail damage, the insurance payout can be the difference between a protected home and a massive financial burden.

- Total Loss on Multiple Slopes: If an adjuster identifies significant "hits" on all four slopes of your roof, you are likely looking at a "total loss" scenario where the math heavily favors filing a claim.

The "Threshold" Test: A Rule of Thumb for DFW

How do you know if your roof damage is worth claiming? We suggest the "Double Deductible Rule." If the total cost of the repair is not at least double your deductible, you should strongly consider paying out of pocket. For example, if your deductible is $5,000 and the roof repair is $7,500, you are only gaining $2,500 in insurance money. The risk to your future premiums and insurability is generally worth more than $2,500. However, if that same repair is $15,000, the $10,000 benefit clearly outweighs the risks.

The Hidden Costs of Filing: Insurability in 2026

In the 2026 Texas market, insurance companies are looking for any reason to "shed risk." We are seeing a record number of non-renewals for homeowners with multiple claims. If you file a small roof claim now, you may find it impossible to get affordable coverage if you decide to sell your home or if you experience a more severe loss later. A "clean" claim history is a valuable asset — sometimes more valuable than the cash payout for a few shingles. This is the claim vs cash pay reality that many "storm chasers" won't tell you.

The Long-Term Impact of CLUE Reports

The CLUE (Comprehensive Loss Underwriting Exchange) report is essentially the "credit score" for your home. Every time you inquire about a claim — even if it's never filed — it can be recorded here. When you go to sell your home in the DFW market, the buyer's insurance company will pull this report. If they see a history of "zero-pay" roof claims, they may refuse to insure the property until a new roof is installed at the seller's expense. This is a massive "hidden cost" of being "claim-happy."

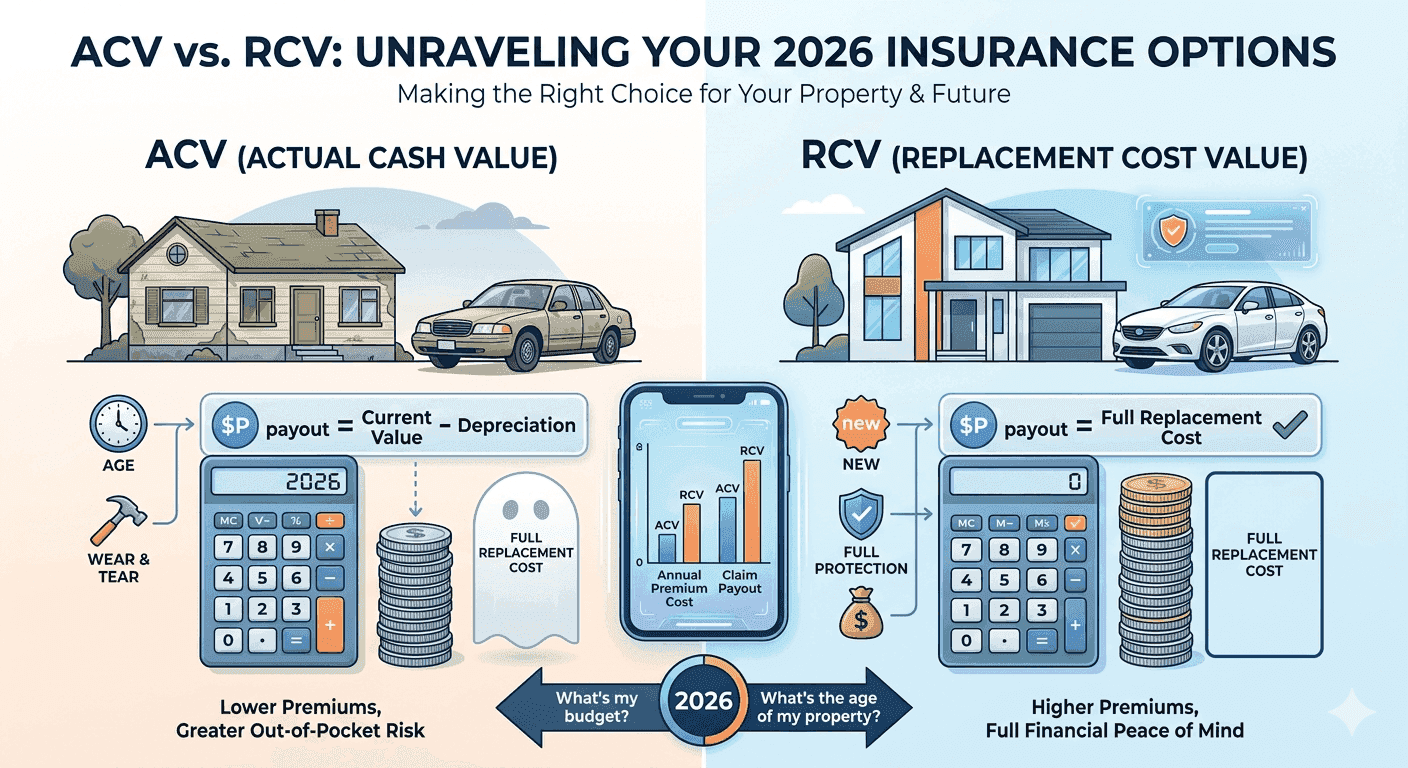

ACV vs RCV: The Policy Type That Changes Everything

Consider the Actual Cash Value (ACV) vs Replacement Cost Value (RCV) distinction. If you have an ACV policy, the insurance company will deduct depreciation from your payout. For an older roof, this could mean they pay out almost nothing after your deductible is applied. In this scenario, the is roof damage worth claiming answer is almost always a resounding "No." You are better off saving that "claim credit" for a true catastrophe and negotiating a cash-pay price with a local contractor who can offer you a "fair weather" discount. Strategic homeownership in North Texas means treating your insurance policy like a "break glass in case of emergency" tool, not a maintenance plan.

A Warning on "Deductible Financing" Scams

Finally, we must address the "deductible financing" scams. If a contractor offers to "waive" or "cover" your deductible to make the claim "free," they are committing insurance fraud under Texas HB 2102. This can lead to your claim being denied and potentially legal trouble for you. Always choose a path that is legally sound and financially prudent. Whether you choose to file a claim or pay out of pocket, ensure your contractor provides a detailed, written scope of work and follows all local DFW building codes. The integrity of your roof is the integrity of your home.

Conclusion: Knowledge Is Power

The decision of "should I file a roof claim" should never be made in a state of panic after a storm. It is a business decision that requires a calm look at your policy, your deductible, and the actual state of your roof. At RoofDog, we provide the honest, technical data you need to make that decision. We don't push claims because we want to be your roofing partner for the next thirty years, not just the next thirty days.

Before you call your agent, call a trusted local expert. Let us map the damage, provide a realistic cash-pay estimate, and help you run the math on whether that roof deductible is truly worth it. Your home is your biggest investment — don't let a hasty insurance claim compromise its future.

Need a Roof Inspection?

Get expert advice and a free estimate from North Texas's trusted roofing professionals.

Schedule Free Inspection