The 2026 Texas "ACV" Insurance Shift: How New Mortgage Rules Affect Your DFW Roof

If you own a home in Dallas-Fort Worth, the ground shifted under your feet in early 2026 — and it had nothing to do with North Texas geology. A quiet but massive change in federal mortgage guidelines from Fannie Mae and Freddie Mac has officially reached the Texas insurance market, and it''s changing how your roof is protected.

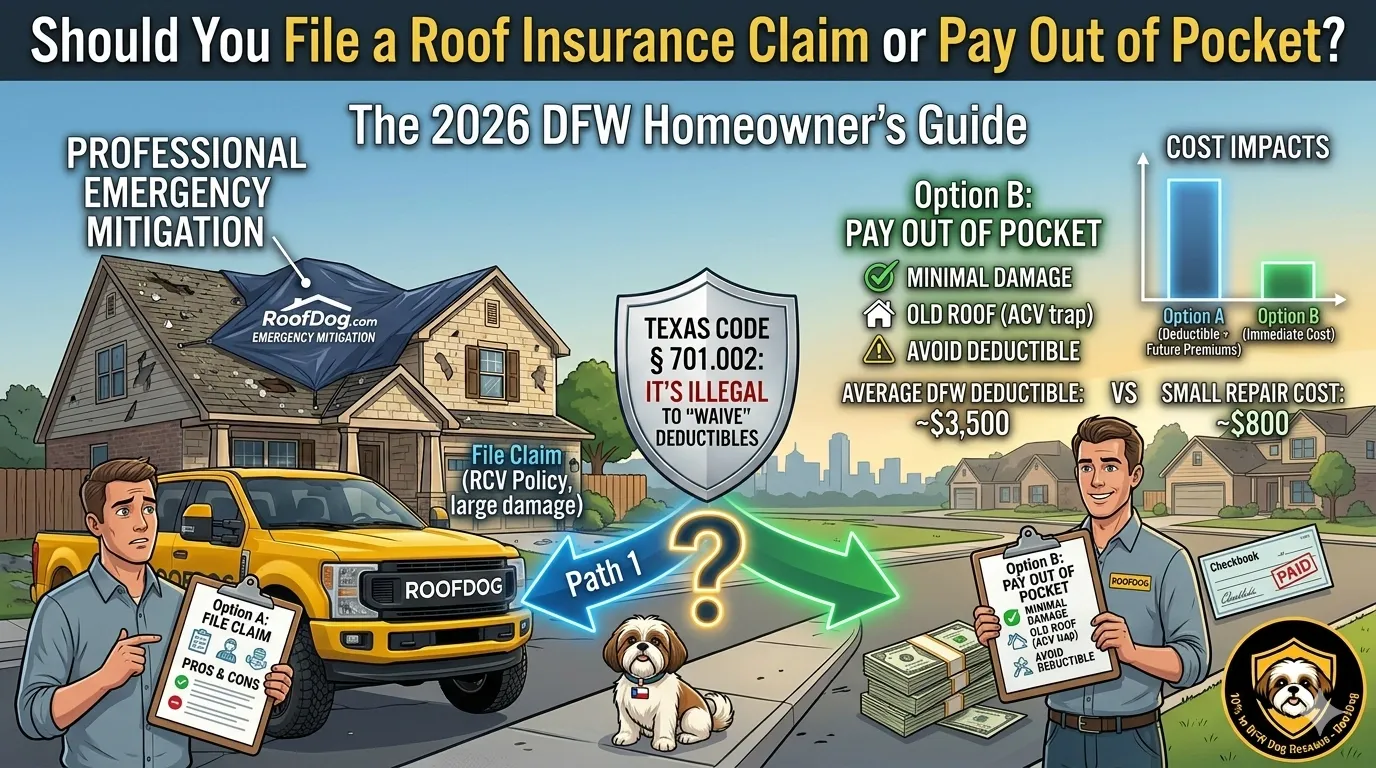

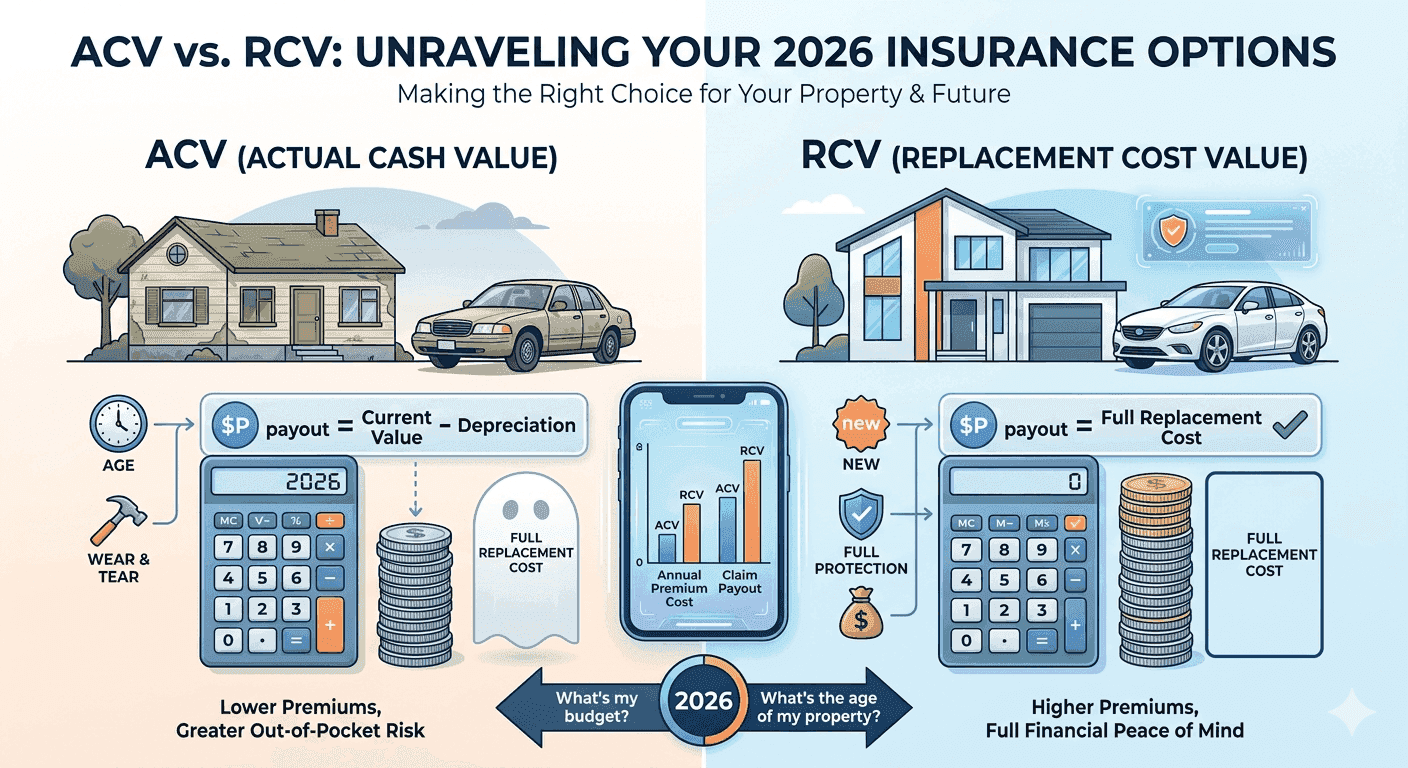

For decades, the Replacement Cost Value (RCV) policy was the gold standard. If hail pulverized your roof, the insurance company paid for a brand-new one. Simple. Predictable. Safe.

But as of March 2026, new regulations have made Actual Cash Value (ACV) policies the "new normal" for many DFW homeowners — and most people don''t realize it until it''s too late.

At RoofDog, we believe in protecting those who can''t protect themselves — whether it''s a senior dog in a shelter or a homeowner getting blindsided by fine print. In this guide, we''re breaking down what these 2026 changes mean for your wallet, your mortgage, and your peace of mind — and what you can do about it.

1. What is the 2026 ACV Insurance Change?

Historically, mortgage lenders required RCV coverage because they wanted to ensure their collateral (your home) would always be restored to full value after a loss. A damaged roof was replaced — not partially reimbursed.

But due to skyrocketing insurance losses across Texas — especially from hail — the Federal Housing Finance Agency (FHFA) updated its guidance. Lenders can now accept policies that use Actual Cash Value (ACV) for roof coverage.

What does ACV actually mean?

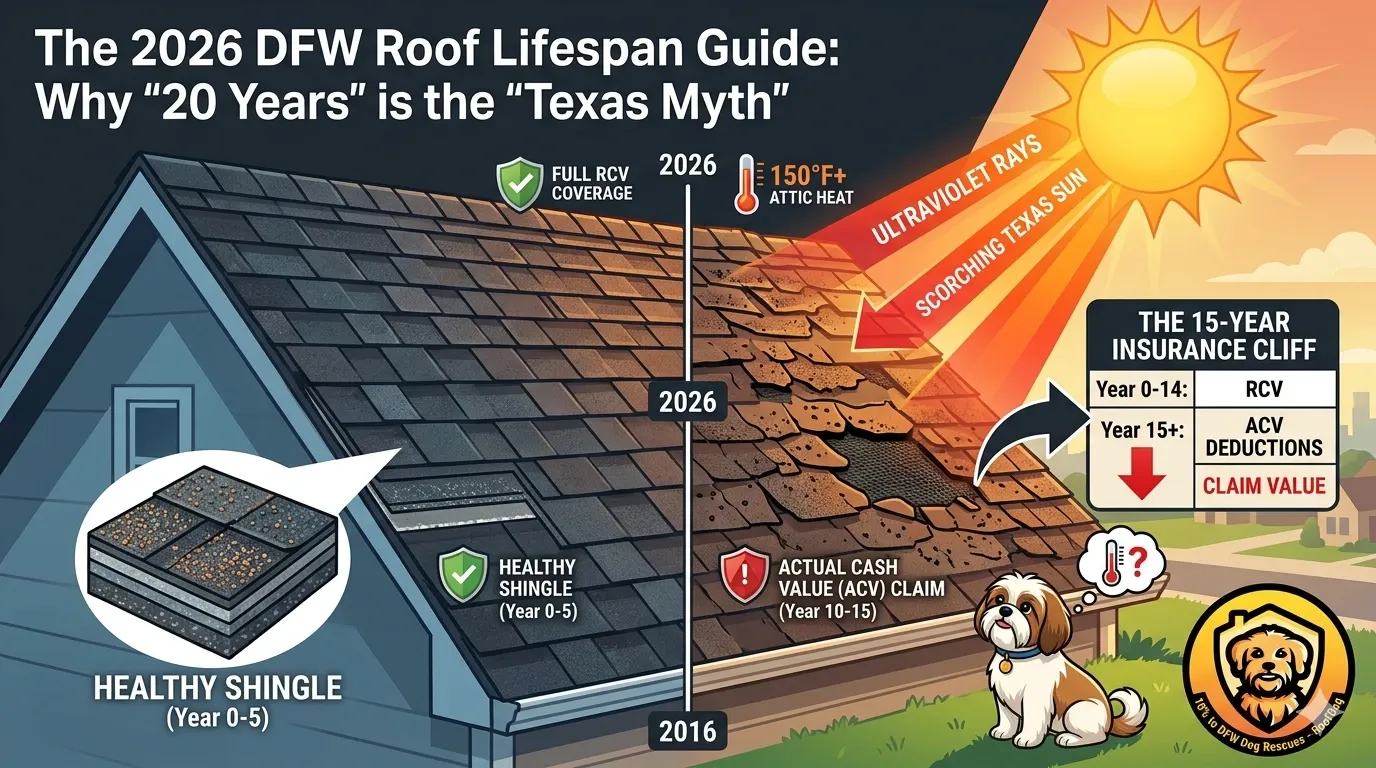

ACV factors in depreciation.

- A brand-new roof: worth full value

- A 10-year-old roof: worth significantly less

- A 15+ year roof: worth very little in insurance terms

Real-world example

- New roof replacement cost: $20,000

- Roof age: 10 years (roughly 50% life used)

- Insurance payout under ACV: ~$10,000

- Your out-of-pocket responsibility: $10,000

That gap is where most homeowners get burned.

2. Why DFW is Ground Zero for this Shift

Dallas-Fort Worth isn''t just a big metro — it''s one of the most active hail zones in the country.

- 2023-2025 saw record-breaking storm activity

- Insurance carriers paid out billions in claims

- Premiums surged across Texas

Carriers responded the only way they could:

- Increase deductibles

- Restrict coverage

- Push ACV policies

Translation: They''re shifting risk from themselves… to you.

In areas like Frisco, McKinney, Plano, and Prosper, many "affordable" policies now:

- quietly include ACV roof coverage

- include depreciation schedules

- dramatically reduce payout potential

Most homeowners don''t notice because the premium looks cheaper.

3. The Hidden Math: Why ACV Feels Fine… Until It Isn''t

ACV policies are often sold as "cost savings." But here''s the reality:

| Scenario | RCV Policy | ACV Policy |

|---|---|---|

| Roof cost | $20,000 | $20,000 |

| Insurance pays | $20,000 | $6,000-$12,000 |

| You pay | Deductible only | $8,000-$14,000 |

The difference isn''t small — it''s financially disruptive. And it gets worse with age:

- 5-year roof → decent payout

- 10-year roof → major gap

- 15-year roof → almost no meaningful coverage

4. The Mortgage Trap: What Most People Miss

Here''s where things get dangerous. While Fannie Mae and Freddie Mac now allow ACV in some cases, your specific lender may not.

If your lender determines your coverage is insufficient, they can:

- flag your loan

- require proof of better coverage

- force-place insurance

What is force-placed insurance?

- more expensive

- less protective

- completely out of your control

Example: You save $600/year switching to ACV… but your lender force-places a policy costing $2,500/year. Net result: you lose money and coverage.

5. How to Spot "The Dog in the Fine Print"

These policies aren''t labeled "bad." They''re labeled:

- "competitive"

- "updated"

- "cost-effective"

Here''s what to look for:

1. "Actual Cash Value" for Wind & Hail

This is the biggest red flag. If your roof is not covered at RCV, your financial exposure is massive.

2. Roof Surface Payment Schedule

This is a chart buried in your policy that looks harmless. It tells you how much your roof is worth (to them) based on age.

Example:

- 5 years old → 70% coverage

- 10 years old → 50% coverage

- 15 years old → 20% coverage

That means 80% of the cost is on you.

3. High Deductibles (2%-3%)

Texas has moved heavily toward percentage-based deductibles.

- $500,000 home

- 2% deductible = $10,000

That is your minimum out-of-pocket before coverage even begins.

4. Cosmetic Damage Exclusions

This one is sneaky. If hail dents metal, bruises shingles, or reduces lifespan — but doesn''t cause an immediate leak — they may deny the claim. Meanwhile, your roof value drops, resale value drops, and future leaks become your problem.

6. The Real Risk: Delayed Damage

One of the most misunderstood issues with ACV policies is delayed failure. Hail damage doesn''t always leak immediately. Instead:

- granules loosen

- shingles weaken

- UV exposure accelerates deterioration

6-18 months later:

- leaks appear

- structural issues begin

At that point your claim window may be closed, your policy may deny coverage, and you pay everything out of pocket.

7. Protecting Your Pack: What You Should Do

If you''re reading this and thinking, "I might have one of these policies" — you''re probably right. Don''t panic. But do act.

Step 1: Check Your Policy Today

Look for ACV language, roof payment schedules, deductible percentage, and exclusions. If you don''t understand it — that''s the point.

Step 2: Call Your Insurance Agent

Ask directly:

- "Is my roof covered at Replacement Cost or ACV?"

- "What would I receive if I filed a claim today?"

- "Is there a depreciation schedule?"

Step 3: Call Your Mortgage Company

Ask: "Does my loan allow ACV roof coverage?" Do not assume.

Step 4: Get a Professional Roof Inspection

You need to know the age, condition, existing damage, and remaining lifespan of your roof.

Step 5: Consider Upgrading Your Roof

Class 4 Impact-Resistant Shingles benefits:

- stronger against hail

- longer lifespan

- insurance discounts (often 20-25%)

- better eligibility for RCV policies

This can offset premium increases while improving protection.

8. The RoofDog Advantage

At RoofDog, we''re not just replacing roofs — we''re helping homeowners navigate a system that''s becoming more complicated by the year.

Our "Post-2026 Policy Audit"

With every free inspection, we can:

- review your roof condition

- help interpret your insurance policy

- estimate your real financial exposure

- recommend next steps

No guesswork. No surprises.

9. The RoofDog Mission: More Than Just Shingles

Why do we care so much about this? Because we''ve seen what happens when homeowners get blindsided. A $10,000-$15,000 unexpected expense isn''t just inconvenient — it''s life-disrupting.

At RoofDog, we believe business should do more than generate revenue. It should do good. Every time we replace a roof in DFW, 10% of our profits go directly to local dog rescues — including Dallas Animal Services and Operation Kindness.

When you choose RoofDog, you''re not just protecting your home. You''re helping rescue abandoned dogs, fund medical care, and support adoptions. A strong roof. A stronger community.

FAQ: 2026 DFW Roofing Insurance

Can I still get an RCV policy in Texas?

Yes — but it''s becoming more selective. Many insurers require newer roofs, higher-quality materials, and better inspection reports.

Is ACV always bad?

Not necessarily — but it''s high risk if your roof is older, you don''t have savings set aside, or you assume full coverage.

How do I know if my roof has hail damage?

You often can''t from the ground. Signs may include granule loss, soft spots, or minor discoloration. Only a proper inspection reveals the truth.

Does RoofDog''s donation cost me extra?

Never. The 10% comes from our profit — not your price.

Final Thought

The 2026 ACV shift didn''t make headlines — but it should have. Because it fundamentally changed the question from:

"Am I covered?"

to:

"How much of this am I actually paying myself?"

The difference can be tens of thousands of dollars. The good news: you''re now aware. And awareness is where protection begins.

Ready to Protect Your Home (and Help a Local Rescue)?

Schedule your free "Paws-on-the-Roof" inspection today. Visit RoofDog.com or call us directly. Let''s make sure your roof is as loyal as your best friend.

Need a Roof Inspection?

Get expert advice and a free estimate from North Texas's trusted roofing professionals.

Schedule Free Inspection